Superannuation is one of the most powerful — and misunderstood — parts of Australia’s retirement system. While most Australians know they have a super fund, fewer truly understand how it works, how much control they have, or how small strategic decisions made today can significantly improve their retirement outcomes.

Whether you’re early in your career, running a business, or approaching retirement, understanding superannuation — and how to use it effectively — is essential to building long-term financial security.

What Is Superannuation?

Superannuation (or “super”) is a long-term investment structure designed to help Australians save for retirement. For most people, super is funded through compulsory employer contributions, known as the Superannuation Guarantee (SG), along with any personal contributions you choose to make.

Super is taxed at concessional rates compared to most personal income, which makes it one of the most tax-effective ways to invest for retirement. However, super also comes with rules around access, contribution limits, and preservation — meaning your money is generally locked away until you meet a condition of release, such as reaching retirement age.

Why Superannuation Matters More Than You Think

For many Australians, super will become their largest financial asset outside the family home. Yet it’s often treated as “set and forget”.

Over a working lifetime, the combination of:

· regular contributions

· compound investment returns

· tax concessions

can create a substantial difference in retirement lifestyle. Two people on similar incomes can retire with very different outcomes depending on how well their super is structured and managed.

Essential Superannuation Strategies to Consider

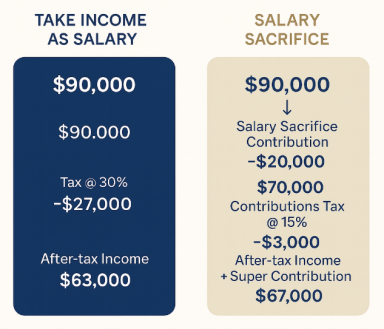

1. Making the Most of Concessional Contributions

Concessional (before-tax) contributions — including employer contributions and salary sacrifice — are taxed at just 15% inside super (subject to caps). For many people, this is significantly lower than their marginal tax rate.

If you haven’t used your full concessional cap in previous years, you may also be able to access carry-forward contributions, allowing you to top up super and potentially reduce tax in high-income years.

This strategy can be particularly effective for business owners, professionals, or anyone with fluctuating income.

2. Reviewing Your Investment Strategy

Your super isn’t just a balance — it’s an investment portfolio.

Many Australians remain in default investment options that may not align with:

· their age

· risk tolerance

· time to retirement

Ensuring your super is invested appropriately for your stage of life can have a meaningful impact on long-term returns. For example, someone with decades until retirement may benefit from a different investment mix than someone planning to retire in the next five years.

3. Managing Fees and Insurance Inside Super

Fees and insurance premiums inside super are often overlooked, yet they can quietly erode returns over time.

It’s important to regularly review:

· investment fees

· administration costs

· default insurance cover

In some cases, holding multiple super accounts or outdated insurance policies can significantly reduce the effectiveness of your retirement savings.

4. Understanding Contribution Types and Limits

Super contributions fall into different categories, each with its own rules and caps. These include:

· concessional (before-tax) contributions

· non-concessional (after-tax) contributions

Understanding how these work — and how to combine them strategically — can help you build super more efficiently while staying within ATO limits.

For couples, contribution strategies can also be used to help balance super balances over time, which may improve flexibility and tax outcomes in retirement.

5. Planning Ahead for Access and Retirement Income

Superannuation doesn’t end at retirement — it changes phase.

Moving from accumulation to retirement income streams involves important decisions around:

· tax treatment

· drawdown strategies

· investment risk

· interaction with the Age Pension

Planning this transition early can help avoid unnecessary tax and ensure your super supports the lifestyle you want in retirement.

Superannuation Is Not One-Size-Fits-All

While the rules around super apply nationally, the best strategies depend on your personal circumstances — including income, employment structure, family situation, and long-term goals.

For many people in Bendigo and Regional Victoria, this might involve balancing business ownership, property, or irregular income alongside super planning. Getting the structure right early can create more options later.

Final Thoughts

Superannuation is more than just a compulsory savings account — it’s a cornerstone of effective retirement planning. With the right strategies in place, super can provide tax efficiency, long-term growth, and financial confidence well into retirement.

If you’d like help understanding how your super fits into your broader financial plan, or whether there are opportunities to improve your position, professional advice can make a meaningful difference.

Let’s see if we can help you.

Contact Greybox Wealth for an obligation-free, no-cost initial appointment and start building a clearer path toward retirement.