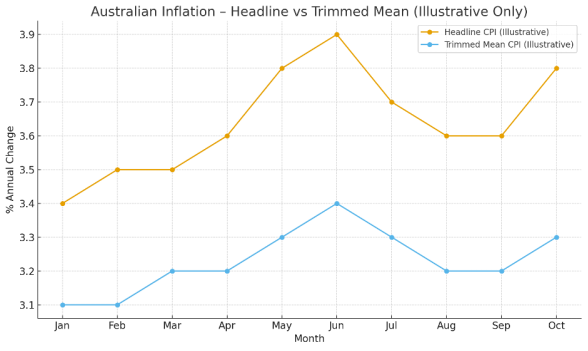

The official Australian Bureau of Statistics (ABS) has reported that for the 12 months to October 2025, the headline consumer price index (CPI) rose by 3.8%, up from 3.6% in the 12 months to September.

Underlying inflation measured by the “trimmed mean” (which excludes volatile items) — also rose to 3.3%.

The main drivers behind the inflation increase were higher costs for housing (including rents and electricity), food and beverages, and broader services.

This hotter-than-expected inflation print smashed market hopes for an imminent interest-rate cut and has renewed expectations that interest rates may remain higher for longer.

What Does It Mean for Retirees

- Erosion of purchasing power: For retirees living off fixed income (from cash, term deposits or conservative investments), inflation reduces what their savings can buy. A larger share of retirement income may be eaten up by rising costs of essentials such as housing, food, medical care, energy and other regular expenses.

- Risk to lifestyle expectations: Over longer retirements, even moderate inflation compounds — what seems manageable now can meaningfully degrade living standards over time if not addressed.

- Need for growth-oriented investments: Retirees may want to lean away from cash/fixed income and consider investments that have historically outpaced inflation (e.g. quality shares, diversified growth assets, or inflation-protected investments) to help preserve real value.

In short: for retirees, this inflation data underscores the importance of reviewing income strategies to preserve purchasing power and avoid being eroded by continuing price rises.

What Does It Mean for Investors

- Higher inflation reduces real returns on cash and defensive assets: With inflation at ~3.8%, holding large cash balances or low-yield fixed income investments becomes less attractive — real returns may be negative once cost-of-living increases are accounted for.

- Equities and growth assets may become more attractive: Over time, shares and other growth assets have the potential to deliver returns that outpace inflation, helping preserve or increase real wealth. Diversified portfolios can also help spread risk across sectors that may respond differently under inflationary pressure.

- Volatility and interest-rate risk remain: Higher inflation increases the risk that central bank policy stays restrictive, which can create volatility in markets — especially for interest-rate sensitive sectors (e.g., property, bonds, some growth stocks). Investors may need to maintain a diversified, balanced approach and avoid over-concentration.

- Defense via diversification and inflation-hedging assets: Including a mix of assets — such as equities, real assets, inflation-linked/alternative investments or global diversification — may help buffer against inflation and reduce the impact of local inflation and interest-rate shifts.

What Should Investors & Retirees Do Now

Given the current inflation environment in Australia, it may be a suitable time to:

- Review your asset allocation and reduce exposure to cash or low-yield defensive holdings.

- Consider introducing or increasing allocations to growth assets or inflation-resilient holdings (e.g. diversified equities, global equities, real assets, ETFs with inflation-hedging potential).

- Ensure your income strategy (especially if in retirement) includes inflation-adjusting or growth-oriented components to preserve purchasing power over the long term.

- Maintain diversification across sectors and geographies to spread risk, especially given higher inflation and potential for interest rate volatility.

Final Thoughts

The latest ABS data with headline inflation at 3.8% and trimmed-mean at 3.3% is a clear reminder that in today’s economic environment, holding large cash balances or staying too defensive in fixed income may erode real wealth over time. Especially for retirees, but also for long-term investors, a balanced and diversified portfolio that includes growth assets or inflation-hedging exposures will likely offer a better chance to preserve real value and income over time.